South Korea’s AI industrial policy meets the energy shock

The collision will not be pretty

AS A MIDDLE Eastern oil shock rocked the world, South Korea’s president sounded a defiant note. “It is as if the ship of the Korean economy…has started to be shaken, and behind those rough seas, a much stronger sea wind is blowing,” said Park Chung-hee. It was 1974, three months after the first Arab oil embargo rocked global markets. Park nevertheless vowed to press on with an ambitious plan launched a year earlier to prop up the sectors, such as heavy machinery and chemicals, that would propel South Korea into the future.

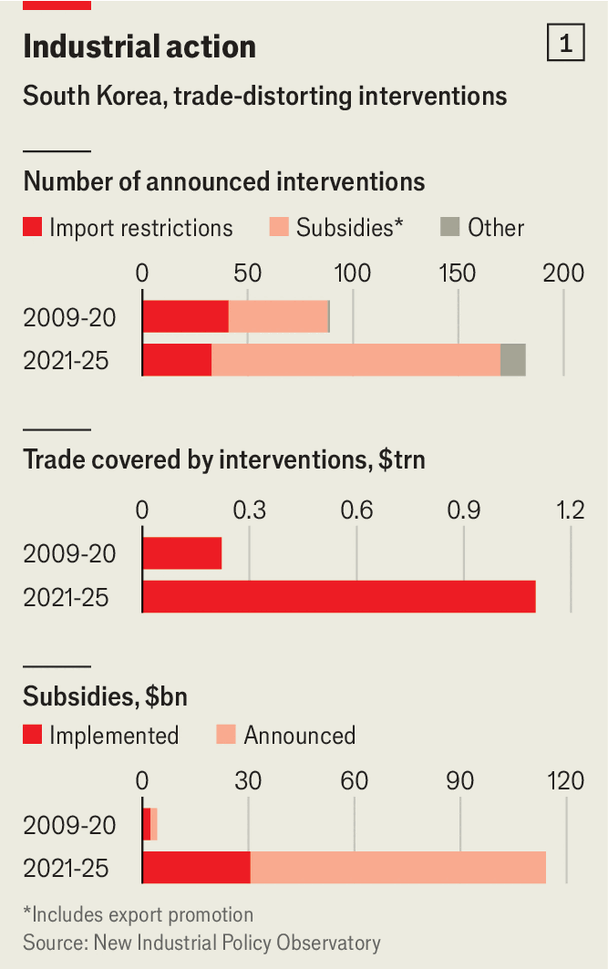

Since then South Korea has forsworn dictatorship. But not industrial policy or tortured metaphors: in November Lee Jae Myung, the newish president, pledged to “construct the highway for the AI era”, just as Park “paved the highway for industrialisation”. His plan involves diverting capital from the housing market to industry, especially chipmakers instrumental to the global artificial-intelligence boom, and supplementing this with government cash (see chart 1). The question is whether Mr Lee can pull it off now that, in another echo of the 1970s, South Korea’s imports from the Middle East, which furnishes 70% of its oil and 20% of its natural gas, are disrupted.

To pave this new highway, Mr Lee envisages spending $530bn over two decades on the chip industry. That is nearly equivalent to a year’s worth of all government spending. He has set up a $50bn fund to, among other things, invest in chip companies’ shares. This government backstop is meant to mobilise another $50bn in private capital. A law passed in January allows the government to channel cash directly to firms via another new off-budget vehicle.

The centrepiece of the vision is the world’s largest semiconductor “mega-cluster” in Yongin City, 40km south of Seoul. Samsung Electronics and SK Hynix, the two giants of domestic chipmaking, have between them pledged $700bn to the project by 2047—a third more than their combined global capital spending over the past decade. The idea is to move beyond memory chips, which Samsung and SK Hynix dominate, and also beyond the chipmaking duo, in order to nurture a broader semiconductor supply chain, less dependent on local and foreign oligopolies. As part of its contribution to the Yongin mega-cluster, for example, SK Hynix is building a “mini-fab”, a chip factory where smaller tool and materials firms can test their products. To distribute the resulting economic gains more widely, Mr Lee has also announced the creation of a semiconductor “belt” spanning three southern cities.

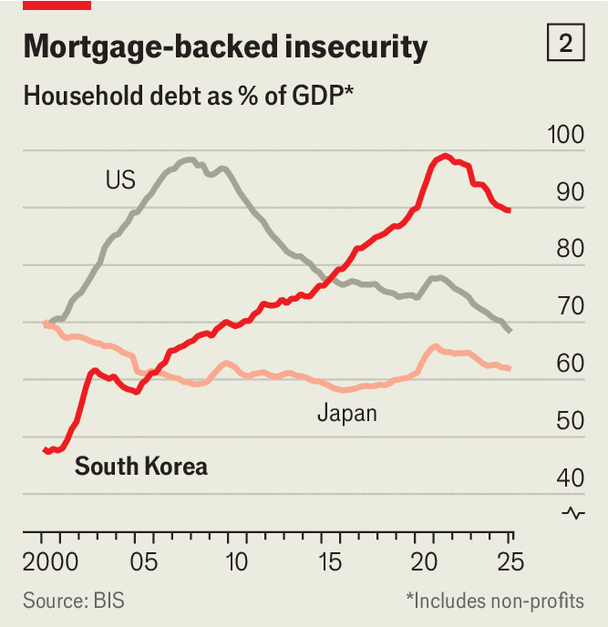

The second plank of Mr Lee’s strategy is to encourage “productive finance”. Too much, in the government’s view, has been flowing, unproductively, into housing. Household debt, much of it mortgage-related, is 90% of GDP, compared with 60-70% in America and Japan (see chart 2). Property prices have soared, particularly in Seoul. The problem is made worse by the jeonse system: instead of paying rent, tenants hand landlords an interest-free loan usually worth over half the value of the property, which is returned at the end of the lease period. The sums tenants borrow to pay for jeonse make up 11% of household debt. Landlords often use the cash to buy other properties, further inflating prices.

To encourage banks to lend less for homes and more to startups, the government is imposing restrictions on housing loans. In swanky Seoul, mortgages cannot exceed 40% of the home’s value, down from an earlier limit of 50% (and compared with 70% in less frothy cities). The absolute value of loans is also limited. On April 1st many caps were extended to mortgages provided by non-bank institutions such as insurers and lending clubs, which have been growing in popularity.

Meanwhile, regulators have reduced the risk weights that banks are required to attach to venture-capital investments, making such bets more attractive. They are also considering lowering these for corporate loans. Banks say this is necessary if they are to lend more to businesses, especially smaller ones. Loan growth to small and middling firms at the country’s four biggest lenders slowed by half last year.

These aims are now colliding with the energy shock. Even if the ceasefire between America and Iran holds, markets will stay disrupted for months. South Korean natural-gas reserves are days away from exhaustion and it will take weeks for new shipments of the liquefied sort from the Gulf to reach Asia. Chipmakers need to be resupplied with other raw materials, such as bromine used in etching (97% of which comes from Israel) and helium to cool silicon wafers (65% from Qatar). Samsung and SK Hynix can cope; they have a few months’ worth of stocks. The startups Mr Lee hopes will flourish may not.

The government is also on the hook for emergency spending. At the end of March it presented a supplemental budget full of support measures, including handouts for low-income families, equivalent to nearly 1% of GDP. Like last year, the budget deficit is above its target of 3% on the government’s preferred measure (which excludes surpluses from big state-pension funds). This may jeopardise its ambitious industrial-policy goals.

The energy crisis is also highlighting the tension between Mr Lee’s chip mega-cluster and his “belt”. The government says redistributing the industry to the renewables-rich south of the country is more important than ever. Critics argue that locating high-tech facilities far from the talent hubs and supplier networks that already exist around Seoul, where 80% of Korean chips are made, makes no sense. As a dictator, Park did not have to deal with such opposition. As a democrat, Mr Lee does. ■

For more expert analysis of the biggest stories in economics, finance and markets, sign up to Money Talks, our weekly subscriber-only newsletter.